The Report illustrates the enormous opportunity of industrial electrification in achieving net-zero targets. Renewable energy development in Canada, however, remains a challenge.

Recommendations to address this challenge are summarized below and outlined in further detail in Section 4 of the Report.

- Review and refine current policies to facilitate easier, more efficient grid interconnections for renewable energy producers.

- Review and modify existing, or create new, incentives for the development and integration of energy storage solutions.

- Re-purpose regulatory frameworks for a more flexible electricity market that facilitates distributed energy resources and new business models.

- Develop new utility models to account for the changing role of consumers to prosumers and the bi-directional communications of the grid.

- Identify regulatory changes required to incentivize utilities to innovate.

- Expand the scope of electricity service operations’ cost guarantee to increase developers’ eligibility.

- Ensure incentives are transferable and stackable with other funding support

- Implement a streamlined process for private or corporate PPAs with producers alongside carbon credits for offtake corporations.

- Implement a two-layer all-in tariff to help increase the certainty of cash flows and thereby enhance equity and debt investor confidence.

- Build a concessional financing platform to leverage low-cost debt financing for on-site renewable energy.

Alberta, which operates under a deregulated Free Merchant Market Model, must contend with price volatility and government uncertainty. According to the Canadian Renewable Energy Association (CanREA), Alberta accounted for more than 92% of Canada’s overall growth in renewable energy and energy-storage capacity in 2023.

Alberta, which operates under a deregulated Free Merchant Market Model, must contend with price volatility and government uncertainty. According to the Canadian Renewable Energy Association (CanREA), Alberta accounted for more than 92% of Canada’s overall growth in renewable energy and energy-storage capacity in 2023.

In August 2023, however, the province announced a moratorium on all new renewable energy projects. While this moratorium does not impact approved projects, it will put projects with potential to come online in 2025 and beyond at risk.

CanREA lists Ontario as the province with the largest installed capacity and, while no new projects came online in 2023, the Association expects capacity to increase with energy storage.

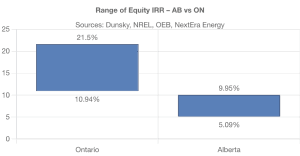

Political uncertainty is the greatest risk for investment in Alberta, which otherwise enjoys strong fundamentals. Renewable energy projects could tap into the more mature carbon markets in the province. With the expected increase in carbon prices to $170/tCO2e by 2030, these projects could present a compelling investment opportunity, providing more lucrative opportunities for solar photovoltaic (PV) than other jurisdictions. Using assumed capacity factors of 20.0% and 22.0% and CAPEX of $1,450/kW and $1,500/kW for Ontario and Alberta, respectively, the equity IRR was compared for the two hypothetical 100 megawatts (“MW”) solar power plants.

The greater potential for strong IRR in Alberta compared to Ontario for renewable energy investments is likely due to a more favorable market structure for competitive energy pricing and a less saturated renewable energy market. While Ontario has strong renewable energy availability, Alberta benefits from high solar irradiance and strong wind profiles, which can result in higher energy output and profitability. Alberta’s favourable investment potential is also supported by a deregulated energy market, which allows for competitive pricing that potentially results in higher returns for investors. Ontario’s fixed returns, while less risky, are less profitable. Ontario’s earlier saturation of the market compared to its grid capacity may also result in reduced opportunities for high IRRs compared to Alberta, where the renewable market is less mature and rapidly expanding.

Ontario’s market is likely to shift with the need to increase electricity capacity.

Transmission and Distribution Infrastructure

Transmission and Distribution (T&D) infrastructure presents a critical bottleneck in the deployment of renewable energy projects. Existing grid infrastructure has limited capacity to integrate and manage the variable and decentralized nature of renewable power sources such as solar and wind. Current grids also are not designed for the bidirectional flow of electricity characteristic of distributed renewable systems such as rooftop solar. Policy and regulatory frameworks must evolve to support faster grid integration of renewables. Without addressing these T&D infrastructure challenges, renewable energy project delays are likely to continue, hindering progress towards clean energy goals.

The University of Toronto’s Climate Positive Energy (CPE)’s $23 million Grid Modernization and Testing Centre provides unique testing capabilities for the Canadian electrical energy industry to help in the evolution to a more decarbonized, decentralized, and digitalized power system. Its objective is to address the market capacity gap through technology testing and real time simulation of various grid models. Micro-grid connections to renewable energy in rural areas specifically in Northern communities is another important aspect that the centre will service through its modelling capabilities.

The transformation of the electricity sector presents a wealth of career development opportunities.

Collaboration

For historically marginalized communities, the shift towards sustainable and renewable energy sources can mean not only jobs but also pathways to long-term careers and leadership roles. Opportunities extend beyond simply participating to actually shaping the new energy landscape. New roles include policy and advocacy positions to guide the electricity sector’s regulatory and ethical compass in ensuring it meets the needs of underserved populations. Opportunities for entrepreneurs will also grow to help launch and scale energy-focused businesses.

Recognizing these opportunities, and the fact that electrification in Canada relies on lands and resources to which Indigenous nations are rights-holders, the First Nations Major Projects Coalition (FNMPC) and Mokwateh partnered to create a National Indigenous Electrification Strategy to “position Indigenous nations as leaders of Canada’s net zero transition and remove economic, political, and regulatory barriers to support and promote the development of Indigenous-partnered and -led clean energy projects in Canada”. The Transition Accelerator’s Electrifying Canada also supports ”sustained collaboration” among power producers, regulators, system operators, industry, organized labour, Indigenous organizations, financial institutions, and civil society to eliminate identified barriers to accelerated electrification.

Transformation Culture

In the wake of the pandemic, many people have forgotten that cities can and should be more than just centers of work and habitation. Designed correctly, they become engines of innovation, propelling economic growth and social evolution. They house commercial activity, leading universities, and research institutions that generate cutting-edge knowledge and attract global talent, building a community of practice that transcends knowledge into craft by putting theory into action, sharpening practical skills through shared experience and dialogue. Individuals expand their ideas through chance encounters on the streets or the various knowledge-sharing and ideation collective hubs and events. This collaborative environment fosters an instinctive understanding of which approaches are likely to succeed and which may falter, informed by the collective wisdom and diverse perspectives of the group.

Strategic Planning

One key challenge in appropriately allocating capital to an equitable energy transition in Canada lies in how the country decides to define and articulate its vision. Critics often characterize Canada’s business environment as an oligopolistic hegemony, which potentially leads to less favourable conditions for employees, consumers and other stakeholders due to a lack of competitive pressure. Those who support Canada’s current economic environment believe that industry consolidation is an imperative for global investment (e.g., favourable to shareholders).

This difference in approach highlights a fundamental debate about the role of government in the economy: Whether to protect certain industries considered vital for national interest and ensure stability through regulation or to promote an open competitive market environment that encourages companies to innovate and differentiate themselves independently. A clear strategic vision for determining which industries need government-protected competitive advantages, and when these protections should be lifted to foster technological progress and economic growth, will support the development of long-term, non-partisan policies designed to increase Canadian innovation and productivity.

Climate change and other global challenges – war, political polarization, inflation and the after-effects of the pandemic – make for an uncertain world and uncertain markets. In Canada, continuing dependence on oil, unclear carbon pricing policies and cancellation of renewable energy programs contribute to continuing uncertainty in industry, in capital markets and among international observers.

Climate change and other global challenges – war, political polarization, inflation and the after-effects of the pandemic – make for an uncertain world and uncertain markets. In Canada, continuing dependence on oil, unclear carbon pricing policies and cancellation of renewable energy programs contribute to continuing uncertainty in industry, in capital markets and among international observers.

The

The